For many years, we have assumed that we can simply exchange our pay cheque from our employer to one from the government once we reach a magical retirement age.

For many years, we have assumed that we can simply exchange our pay cheque from our employer to one from the government once we reach a magical retirement age.

This is the way it worked for a long time, but there is growing evidence that we need to redefine what it means to retire. Here are four reasons why.

1. The government keeps changing pension and superannuation rules

Currently, to receive the age pension you must be at least 65 and meet the 10-year qualifying Australian residence requirements. Income, assets and other circumstances also affect how much pension you will get.

From 1 July 2017, the qualifying age for the age pension will increase from 65 to 65.5 years. The qualifying age will then rise by six months every two years, reaching 67 by 1 July 2023.

The experience in Australia is by no means unique. Governments in the United Kingdom and Canada are also increasing the age at which their citizens can receive the age pension to 67. And other countries are sure to follow suit.

Also, compulsory superannuation is increasing from the current 9% of salary to 12% by 2017 to meet the government’s estimated funding shortfall, and there is talk about changing the rate at which superannuation is taxed for the wealthy.

Who knows what rules will change next? When our government talks about pillaging superannuation accounts to pay pensions you know that your retirement savings are only truly yours until the rules are next changed.

Perhaps it’s time to consider diversifying retirement savings a little, and there’s bound to be a growing industry dedicated to doing just that. The trick will be to separate the good investments from the bad to avoid being duped, and to get educated on the opportunities that do exist.

2. Longer retirement = more spare time

According to the Australian government, an Australian male born today can expect to live to 79 years, and a female to 85 years. These results place Australians in the top five countries in the world for life expectancies.

In 1900, life expectancy at birth was 55 years for males and 59 years for females. Over the course of a century, life expectancy has increased by over 20 years.

Given medical discoveries and health improvements, it is possible that our life expectancies will increase further in future.

This means that we can expect to have more free time on our hands after retiring, and the burning question will be what to do with it if we don’t want our mental and physical faculties to deteriorate.

We could choose to extend our working lives beyond the official retirement age, but our workforce may have other ideas and push us out. There may be more opportunities to work part time, or we could possibly start all over again in an industry that may only have been fledgling when we began our career journey.

The simple fact is that we can expect to spend at least 20 years in retirement, and this is a lot of spare time to cover, especially if you are still in good health and the kids have fled the roost.

Expect to see more initiatives for retirees to learn new skills, volunteer back to the community or being encouraged to stay on in the workforce.

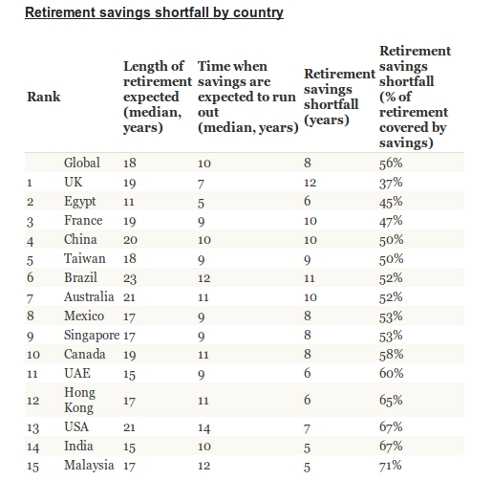

3. You don’t have enough money to do all you want to do

You finally have the free time to do everything you wanted to do only to find that now you can’t afford to, and you are terrified of outliving your savings.

It would be wonderful to consider retirement as a long fully-paid vacation around the world, but the truth is that many of us will be struggling just to make ends meet.

Throw in another recession while you are in the throes of accessing your superannuation and a more comfortable lifestyle post retirement will remain just a dream.

Although sad to admit, many of us will be forced to live on less than we would like. But this doesn’t have to be as restrictive or demoralising as it sounds. The frugality movement has already gained significant momentum around the western world, and it may bring you significant pleasure to find new ways to spend less, grow your own veggies or even do your bit to save the planet.

The baby boomers have always been a resourceful lot, so don’t be surprised to see original ways to live comfortable lifestyles and meaningful lives as budget-busting living become the reality.

4. All or nothing is so old hat

There are strict but confusing definitions around when and how you can access your superannuation savings – as well as the government pension. As a result, many people find it easiest to choose “working” or “retirement” as convenient buckets to define their status – with no middle ground.

The expectations of our society for many decades have reinforced this acceptance we have that we will work until we retire, at which point we go from one extreme to the other.

The middle ground of working some of the time and retiring some of the time needs further exploration.

Wouldn’t it be great if it were easier to work regular part-time hours, or if you could job share so you work only three or four months each year then can travel for a few months and retire for the rest. Or even engage in some new work scheme that eases the government’s pension burden while giving you greater flexibility to take a break when you want one.

It would benefit society as a whole if we could find more flexibility in the middle ground between working and retiring, and it’s time we opened up this treasure chest to generate some new ideas.